AEI just released a report about appraisers coming in below contract price in areas with lower income buyers, lower priced homes and more blacks and Latinos. This is exactly what I've been talking about. Again, AEI proves it with science and facts. Just FYI AEI is considered a "conservative" source.

"Our critique points out some significant shortcomings of these studies. Notably, they focus on entire

neighborhoods, when they should study the actions of individual appraisers. They use the greater share

of under-valuations as evidence of racial bias, when they should consider explanations unrelated to bias

that might account for under-valuations, including for example the greater share of first-time

homebuyers, who tend to overbid, or the greater presence of seller concessions, which will reduce the

appraisal amount when they are properly accounted for. They also fail to note the size of these undervaluations. Using the Aggregate Statistics Data File and Dashboards, our analysis indicates they are relatively small, averaging about $1,100 to $1,900.5 These levels are too high if they are in fact due to racial bias. However, our analysis finds multiple other plausible explanations for under valuations of this magnitude such as the greater presence of first-time homebuyers or seller concessions. We also note

that under valuations of this magnitude of are unlikely to depress entire neighborhoods and, they may

in fact provide a disproportionate consumer benefit to minority homebuyers.

We conclude with a renewed call on Fannie Mae, Freddie Mac, and regulators such as the FHFA to mass screen individual appraisers for racial bias and inaccuracies. We have already laid the groundwork for this research with a published working methodology."

The most important issue which I've stated previously is they focus on appraisal value and contract price for purchases and no refinances. When doing an appraisal for purchase the appraiser NEVER sees, meets the borrower, buyer. We may see the seller or the seller's agent but never the borrower. The government study also doesn't know the race or color of the borrower, buyer AND appraiser. What if it's only black appraisers coming in low with black borrowers? A recent horrible unreliable "study" showed that the appraiser who came in the lowest for black people was themselves black.

More important observations from AEI's study. Contract price does not equal market value. First time home buyers which are more likely in these lower priced areas are more likely to over bid. They don't always know they can negotiate. These same areas tend to have homes in lower condition. The appraiser adds more comps to appraisals which are below contract price. I do this to fully back up my work so everyone can understand the value. An appraisal that comes in below the contract price would not endear you to the AMC or lender. Appraisers HATE coming in below contract price but we do it because it's the right legal fair thing to do. The appraisal is to secure the loan not help a buyer or seller.

Some good snippets though you should read the entire report.

Fist time buyers offer over market value. "Shui and Murthy (2019) conclude that first-time homebuyers using Fannie Mae or Freddie Mac financing overbid for a home by approximately $3,000, or about 1% of the contract price for the average home compared to repeat buyers. They also find that FTBs with higher LTVs tend to overpay by more compared those with lower LTVs. FHA borrowers, who are disproportionally concentrated in minority census tracts and largely FTBs, typically have higher LTVs and lower credit scores and may thus be more likely to overpay than other buyers."

There are more seller concessions in these first time buyers, buyers using gov funding and these areas. If a home sells for $100,000 and has a $3,000 seller concession, appraisers subtract $3,000 from $100,000 in the adjustments. The net price is $97,000 which is under contract price now by 3%. There are more concessions to help buyers buy the property and because of condition.

There are more buyers for lower priced homes. This causes buyers to over bid for homes based on supply and demand. We saw this during the recent Covid runup. Buyers bid and paid over list price. They had to make up the difference in loan amount with a larger down payment.

First time buyers aren't just competing against other buyers but also against their rent. Many only compare what they are paying in rent to what their mortgage will be. Quick story. Friend of mine was buying a cheap mobile home. She wanted to buy a cheap home because the mortgage is less than her rent. She was buying it to save monthly expenses. Appraisal came in $20,000 below contract price of $85,000. She asked me for help. I told her appraisal value looked correct. I told her to ask seller to reduce price. She said "but it's actually worth $85,000! It's almost the cheapest house on the market! I will lose the home to someone else! I have to buy this home because the monthly payments are cheaper than my cheap rent!" She didn't care about the price but the monthly payment being less than rent. She only wanted to find a way to get $20,000 more cash for the down payment. Thankfully seller reduced the price. The appraisal gap prevented her from over paying for her first home. Many first time buyers in less expensive areas feel the same way.

Buyers using government funding tend to overbid. They're buying the home with someone else's money because of lower down payment requirements.They just want the home at any price believing it will instantly go up in value and they will have thousands in equity to take eventually. The government told them this is the American dream.

The actual appraisal gap is small. There is almost no gap in Latino areas and 1% in black areas. The government made this huge stink about appraisal gap and there barely is one! "In our prior critique of Freddie Mac’s research note, we find that “there appears to be no gap [in home purchase appraisals] relative to White tracts for Latino tracts and a relatively small gap [in home purchase appraisals] of 1-2% for Black tracts.” They mean predominantly white, Latino or black census tracts. None are 100% white, black or brown. That means whites are having the same issues in those areas as blacks and Latinos. The gap is not a color issue because the same things happens to whites in the same area.

AEI again debunks Andre Perry's "paper." Perry stated appraisers devalue black owned property by $48,000 per home. That's much more than the difference in contract price and appraised value of 1%. AEI pointed out that homes owned by poor whites are also valued less than homes owned by wealthier whites. It's not because of skin color but income, wealth and location.

Appraisals coming in below contract price can help lower income Latino, black buyers. They can renegotiate with the seller. The government didn't say the buyers never closed on the properties and the deals died. They're prevented from overpaying and ending up upside down. AEI state that the government is part of the problem. They help and allow buyers to over pay for homes at the top of the market only to lose those homes later when the market tanks or they have a financial emergency. And you know who the government falsely blames for that? Appraisers!

This kind of reminds me of the destroyed apartment buildings in the Turkey earthquake. Their President bragged that he reduced earthquake requirements to allow the construction of 300,000+ homes for lower income people. That is one of the major causes of the high fatalities in the earthquake. The President basically killed people. FHA and the government like to brag that they helped low income people buy homes. Then they lose their homes because they over paid at the peak of the market and couldn't easily pay the mortgage. Also reminds me of our student loan problems. Latinos, blacks are the ones stuck with huge student loans while the government brags they helped them get an education. Most didn't even finish their education and get the degree or certificate. Most of the ones that did didn't even get the better paying promised job. Governments just want to brag that they "helped" people not caring that they actually destroyed them financially. If the government helped them find a way to earn more money, they could buy a home on their own and afford to stay in it.

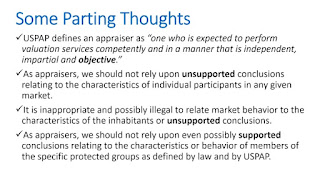

AEI suggest mass screening of appraisers to check for racial bias. I support this. If any appraiser knew of a racist appraiser who came in low on a black, Latino owned home because of their racial bias, they would love to take that appraiser back behind the wood shed. All appraisers are being attacked, vilified, defamed based on this false narrative of the "racist old white male appraiser." While racism sure as hell exists, not all appraisers are racists who lowball Latinos and blacks. If there are appraisers doing this, other appraisers would be the first to hold them accountable and strip them of their license.

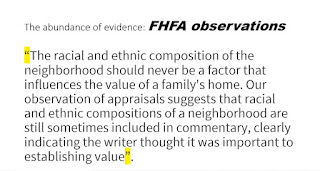

FTR Dan Wiley of Freddie Mac stated this about their appraisal gap research. "We have not reached any conclusion for cause of the gaps or correlation. Our research showed that further studies are warranted." Danny Wiley and Freddie Mac are doing further research into the possible causes of the appraisal gap. They are looking at all the new data and reviewing all appraisals involved in the appraisal gap research. Of course that hasn't stopped Marcia Fudge, HUD, media... from running with Freddie Mac and other's inconclusive data about appraisal gap from stating it's allegedly caused by racial discrimination by appraisers.

Mary Cummins of Cummins Real Estate is a certified residential licensed appraiser in Los Angeles, California. Mary Cummins is licensed by the California Bureau of Real Estate appraisers and has over 35 years of experience.

- Mary Cummins LinkedIn

- Mary Cummins Meet up

- Cummins Real Estate on Facebook

- Mary Cummins Real Estate blog

- Cummins Real Estate on Google maps

- Mary Cummins of Animal Advocates

- Mary Cummins biography resume short

- Mary Cummins Real Estate Services

- Animal Advocates fan page at Facebook.com

- Mary Cummins

- Mary Cummins Animal Advocates on Flickr photos

- Mary Cummins Animal Advocates on Twitter.com

- Mary Cummins on MySpace.com

- Mary Cummins on YouTube.com videos

- Mary Cummins of Animal Advocates on Classmates

- Mary Cummins on VK